See why 4thWay now accepts ethical ads.

How To Pick P2P Property Development Loans

Development loans offer attractive interest rates of 8% or more, secured on land and property, so they are appealing to lenders.

Development loans offer attractive interest rates of 8% or more, secured on land and property, so they are appealing to lenders.

Most property P2P lending websites focus on development loans more than other kinds of property loans.

(See sidebox, right, to find out what development loans are.)

We've written before about why property development lending is riskier than most. I suggest you read those articles first and then come back to this one.

Why pick individual loans?

Ultimately, the best ways to be safe is to satisfy yourself that the people working at the P2P lending site are competent, and then you spread your money across lots of loans and lots of P2P lending sites.

That is much more important than investigating every property loan in detail.

But, if you're thorough, part of assessing the site in general could mean looking into at least one of its loans. Plus, you learn more about what you're doing which enables you to lend with more confidence. With confidence, you might feel comfortable reducing your number of loans and picking those with lower risk and higher returns.

How to assess one development loan

There are never-ending details you could look into, such as the flood risk or looking for contamination reports and much more.

But below I have tried to boil it down to the most important points that you could probably do in about half an hour if you're feeling wide awake. You might then trust the site more in future so that you don't always need to read all these details.

To take you through this, I'm going to show you how I quickly gave a deal on the Relendex* website the once over.

The basic loan information

The Relendex loan I'm looking at today is “Buckinghamshire Residential Development”, which is the last one to go live on the site.

The headline details of the loan are:

- Loan amount: £300,000.

- How long it is expected to last: 12 months.

- Lending interest rate: 8.75%.

- Loan-to-value (LTV): 67%.

(See sidebox, right, for explanation of LTV.)

Check the LTV

The Relendex site also shows that the property valuation is £450,000, which is where the 67% loan-to-value (LTV) comes in:

£300,000 loan and a £450,000 valuation means the loan is 67% of the property valuation.

On a calculator you simply type 300000 / 4500000 = 0.6666666667, which rounds to 0.67 which means 67%.

Loans-to-value aren't always straightforward, so you need to do some checks.

Relendex provides registered lenders access to many of its documents related to the loan – as it should do.

This includes an independent property valuation from a RICS surveyor. I downloaded that and all the other documents and virus-scanned them before opening them.

The RICS report shows that the £450,000 figure is what the surveyor believes the property will be sold for when the development has been built and completed in about 8-12 months' time.

This is called the gross development value. (“Gross” in that phrase means the total price before deducting, e.g. the sale fees that you'll pay to the estate agent.)

Most P2P lending sites doing development loans measure the loan-to-value against this future, hoped-for sale price not the current price that the property should get if sold today. That's normal.

But clearly it means there are more risks, e.g. because it might cost more to build the property than expected or the property might sell for less.

Check the property was physically inspected by RICS

What you probably want to see is that an independent RICS surveyor has done a full physical inspection, i.e. they actually visited the site.

That's what happened here with Buckinghamshire loan, according the RICS report.

The alternative to a site visit is a desktop valuation, which means the RICS surveyor would use websites like Rightmove to estimate the value, without measuring the site or inspecting its condition.

In some rare cases, desktop valuations might not be conducted by independent RICS surveyors, but by someone in the P2P lending site's own team.

Relendex has had at least one desktop valuation done by a RICS surveyor. Desktop valuations are probably only appropriate when the loan required is way, way smaller than the valuation, so that there's a lot of comfortable space for error.

When was the valuation done and the property inspected?

The RICS property valuation document is dated August 2017. Also, the physical inspection must have been in August, because Relendex only asked the surveyor to do the report earlier that same month.

Relendex approved the loan to go ahead in the same month, so the report is up-to-date.

You should expect the LTV to be better (lower) for old valuations, because they are less reliable today.

How much is the current site valued at?

The RICS report puts the site value now at £165,000 to £175,000.

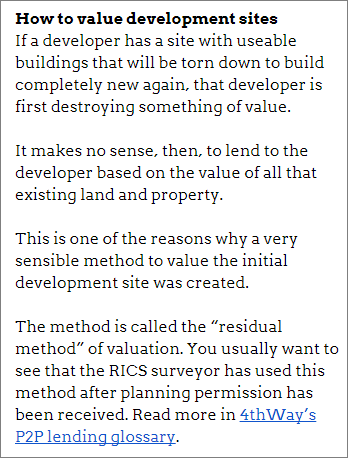

Has the developer used the residual method to value the current site?

Has the developer used the residual method to value the current site?

The short answer for this Buckinghamshire loan is Yes, according to the RICS report.

The residual method is an effective way to value the current development site, i.e. before the development goes ahead.

If the RICS surveyor did not use the residual method, you might need to look into the valuation in more detail yourself.

This is particularly so if the developers are going to swing the wrecking ball on an existing property before building anew.

(Which they aren't in this Buckinghamshire loan.)

Please read the sidebox to the right if you want a summary of the residual method and why developers use it. Click on the sidebox if you want to read even more details about it.

Are you first in the queue to get your money back?

In Relendex's case, I looked at another of its loan documents called the “Loan Proposal” and found the answer is Yes. If the property needs to be repossessed and sold to recover bad debt, the Relendex lenders in this loan will get their money back before anyone else, even if the borrower owes Barclays, MBNA and a dozen other banks.

What you're looking for is whether you have the “first charge” or that the property is “held in trust”. Either of those show you're ranked first.

There's nothing wrong with second or third charge loans, but since the risks are higher you need to learn a bit more about what you're doing first.

Is the loan being paid out in tranches?

The current valuation is £175,000 but the loan is £300,000.

So the next thing I looked for is whether the loan is being cut up into portions to be fed to the borrower. In Relendex's case, I looked at another of its loan documents called the “Loan Proposal” and found the answer is Yes.

The loan proposal states that each portion is only given to the borrower after a monitoring surveyor hired by the P2P lending site certifies that the most recent construction phase has been completed satisfactorily. (This surveyor is on top of any building monitors sent by the local council.)

When the borrower completes a phase of work, the existing value goes up. The P2P lending site can therefore more safely allow the borrow to “draw down” more of the loan.

In the case of Relendex, the borrower has to pay interest on the whole loan even when Relendex hasn't released all the tranches to the borrower yet. So lenders are due interest on money that the borrower isn't even allowed to spend yet. Nice.

Some other P2P lending sites do it differently. They ask lenders to lend the first tranche amount and then they ask for more cash in following tranches when the developer needs it.

Is the loan-to-value capped?

In the loan proposal document, I looked for the word “covenant” and found it, which said the covenant is a 67% loan-to-value.

No further details are provided, so I'll assume that this means a basic covenant whereby the loan to the borrower cannot exceed 67% of the hoped-for sale price. If the sale price is reassessed downwards then the borrower might not receive all tranches or might even have to repay some of the borrowed money early.

What I hope the covenant also means, but it is not specified, is that the borrower also cannot drawdown more than 67% of the current value of the property at each stage of development. This would mean the borrower would not receive more than £117,000 early on.

What stage is this development at?

It's clear from the RICS report that this Relendex loan is at the post-planning, pre-construction phase.

In other development loans, you'll find that some stages of the construction work have already been completed and you have the opportunity to get into the loan at a later stage. Alternatively, the development is just adding to an already extensive building.

The RICS report on this Buckinghamshire loan states that the developers have received planning permission already (which can greatly increase the value of a site and removes one item of uncertainty.)

If a borrower is getting a loan on a site before planning permission is granted, I don't consider this to be a development loan, but some P2P lending sites do classify these as development loans, so watch out for that.

Another key stage is when the groundworks are done, because developers usually only find out for sure how hard it is to build on a site after they have got stuck into the foundations.

The closer to completion, the less risk you are taking by lending, because less can go wrong.

Is it a simple property?

Does the valuation report show it to be a straightforward property? In this Relendex loan, yes it does.

It's a standard brick house with PVC windows and gas-central heating. The RICS surveyors' view is that it is good for homeowners, landlords, developers and other buyers.

The more unusual the development, the riskier it will be. In that case, you might want to see either incredibly low loans-to-value or that the P2P lending site has sent a quantity surveyor or architect to more closely assess the difficulty of the build and the building costs.

Have solicitors looked into it?

While the RICS surveyors do a basic Land Registry search and mention the results in the valuation, you want lawyers to look into ownership and land-usage rights in more detail, and to see if there are any enforcement notices, which would mean the local council thinks there's been a breach in planning control.

Relendex does not attach a solicitor's report, so I checked its loan proposal document. It states that: “The title to the property will be reviewed and reported on for the benefit of the lenders by panel solicitors.”

Despite that note, I can find no report from Relendex about whether the solicitors looked into the matter and what the results were. Personally, I would probably email Relendex to confirm the results before lending. I don't really doubt that they have done it, but I would want to nudge them to be more thorough in future.

Are the borrowers experienced?

Relendex does not attach any evidence, but in its loan proposal it states that the developers are a husband and wife team with lots of experience, including 10 completed development projects, and at least one of them is a new build.

Some of these completed developments they have kept themselves to rent out.

The borrowers' financial situation

Again, Relendex attaches no evidence of any legal, credit or other searches, but in its loan proposal it states that Relendex has assessed the borrowers' finances, including proof from an accountant.

The borrowers have a property portfolio worth over £4 million. They have existing property loans and mortgages of £2.25 million, which means they own outright £1.75 million-worth of property. Including their other wealth, they have about £2 million with no other meaningful debts.

So it should be easy for the developers to pay any extra interest due to Relendex lenders, if selling the property takes longer than the planned 12 months.

The developers have three other development sites and these are all likely to be interconnected financially. This means the borrowers get a loan for one development, which frees up money to start another development at the same time, and so on.

Specifically, the loan proposal indicates that the first £100,000 of the £300,000 loan will probably ultimately go towards investing in another development, as opposed to construction works.

This is complexity I prefer not to see, but in reality it is hard to find developments from experienced developers without it.

The developers have provided personal guarantees to repay Relendex lenders out of their own pocket if selling the site doesn't cover the loan repayment. When lots of developments are cross-subsidised, the value of personal guarantees can erode, especially during a property crash.

Without more details on all the other developments they have in the works, we can't really get a strong handle on the strength of this personal guarantee. Still, a lot has to go wrong for these experienced developers before it becomes worthless.

What is the borrowers' exit strategy?

According to Relendex's loan proposal, the borrowers will either get a buy-to-let mortgage to pay off the development loan and keep the property to rent out for themselves, or they will sell the property.

The glance test

Finally, I glanced through the valuation and all the other loan documents to look for any concerns, but I couldn't find any substantial ones.

A checklist based on the above

- Check you have got a long RICS valuation report (should be tens of pages long).

- Was the property physically inspected by the RICS surveyor?

- Check if the loan-to-value is based on the current value or the gross development value (the hoped-for sale value).

- How recent is the valuation and the site inspection?

- Was the residual method of valuation used?

- Are you ranked first to get your money back?

- Is the borrower receiving the loan in tranches?

- Are the tranches approved by a monitoring surveyor appointed by the P2P lending site?

- Is the loan-to-value capped?

- What stage is the development at? (Planning permission received, groundworks up, building up with extension planned…)

- Is it a simple property? (Such as residential, brick, tiled roof, PVC, being good for owners and landlords.)

- Have solicitors given it the once over?

- Are the borrowers experienced?

- Do the borrowers have a strong financial situation?

- What is the borrowers' exit strategy?

- Does a quick glance through all the documents reveal any concerns that leap out at you?

My view

Any loan can go bad and you don't know which ones will. But I believe if you had a lot of loans like this one paying 8.75% interest, from more than one P2P lending site, then your development loans will be in a strong position. Still, please spread your money across other types of loans too, not just development loans.

Read more about assessing loans in:

Checklist For Selecting Development Loans.

How To Assess P2P Lending Websites.

And in our lending guides on our Learn page.

To get the best lending results, compare all P2P lending and IFISA providers that have gone through 4thWay’s rigorous assessments.

Independent opinion: 4thWay will help you to identify your options and narrow down your choices. We suggest what you could do, but we won't tell you what to do or where to lend; the decision is yours. We are responsible for the accuracy and quality of the information we provide, but not for any decision you make based on it. The material is for general information and education purposes only.

We are not financial, legal or tax advisors, which means that we don't offer advice or recommendations based on your circumstances and goals.

The opinions expressed are those of the author(s) and not held by 4thWay. 4thWay is not regulated by ESMA or the FCA. All the specialists and researchers who conduct research and write articles for 4thWay are subject to 4thWay's Editorial Code of Practice. For more, please see 4thWay's terms and conditions.

*Commission, fees and impartial research: our service is free to you. 4thWay shows dozens of P2P lending accounts in our accurate comparison tables and we add new ones as they make it through our listing process. We receive compensation from Relendex and other P2P lending companies not mentioned above either when you click through from our website and open accounts with them, or to cover the costs of conducting our calculated stress tests and ratings assessments. We vigorously ensure that this doesn't affect our editorial independence. Read How we earn money fairly with your help.